Crypto Regulations in India 2026: Legal Status, Tax & TDS Explained

As the crypto market continues to grow, more and more people in India have started investing in cryptocurrency. With this growing interest, the first question that naturally comes to mind is: what are the rules and regulations around crypto in India? Is cryptocurrency legal and safe to use in India?

The confusion exists because crypto in India is neither completely legal nor completely illegal. The government allows people to buy, sell, and hold crypto assets, but at the same time, it imposes strict tax rules, compliance requirements, and regulatory oversight. Many investors enter the crypto market without understanding these rules, which can lead to heavy tax penalties or legal trouble.

The government is closely monitoring digital assets due to concerns such as money laundering, tax evasion, financial stability, and investor protection. At the same time, India is also working with global bodies like the G20 and FATF to create a more structured framework for crypto regulation.

To clear this confusion, I spent time doing deep research on this topic using official sources and government guidelines. In this article my aim is to clearly explain India’s crypto regulations in 2026, including taxation, TDS, and the legal status of cryptocurrencies. Whether you are a beginner, an investor, or someone simply curious about crypto, this guide will help you understand how crypto works in India, what the government allows, and what you must do to stay compliant with Indian laws.

Is Cryptocurrency Legal in India in 2026?

The answer is not a simple yes or no.

As of 2026, cryptocurrency is legal to buy, sell, and hold in India, but it is not officially recognized as legal money. This means Indian citizens are allowed to trade and invest in crypto assets, but crypto does not have the same status as the Indian Rupee.

The Indian government has not banned cryptocurrency. Instead, it has chosen to regulate and tax crypto activities, which clearly indicates that crypto usage is permitted under the law, as long as users follow the rules.

In India, cryptocurrency falls under the regulated category. It is not illegal, but it is tightly monitored through taxation, KYC norms, and reporting obligations.

Supreme Court vs Government Stance on Crypto

In 2020, the Supreme Court of India lifted the RBI’s banking ban on cryptocurrency, stating that a complete restriction was unconstitutional. This judgment allowed crypto exchanges to operate again and gave users access to banking services.

However, the Indian government’s stance is more cautious. While it has not banned crypto, it does not actively promote it either. Instead, the government focuses on:

- Strict taxation

- Anti-money laundering rules

- Investor protection

- Financial system stability

This creates a situation where crypto is allowed, but under strict oversight.

What is the meaning of “crypto is not legal tender”

You may have seen many official statements saying that cryptocurrency is “not legal tender” in India. This line can easily confuse anyone. Honestly, I was confused by it too at first. Not legal tender simply means:

- You cannot use crypto to pay taxes

- You cannot force anyone to accept crypto as payment

- Crypto is not backed by the Indian government

However, this does not mean crypto is illegal. It only means that crypto cannot replace the Indian Rupee as official money. You can still own, trade, and invest in it as a digital asset.

So, by now, you should clearly understand that cryptocurrency is not banned in India. It is legal to hold and trade, but it is regulated and taxed by the government. However, crypto is not legal tender.

Which Government Bodies Regulate Crypto in India?

Cryptocurrency in India is not controlled by a single authority. Instead, multiple government bodies monitor and regulate different aspects of crypto such as taxation, compliance, risk control, and financial stability. This multi-agency approach shows that the Indian government treats crypto seriously, even though it is not legal tender.

Role of the Ministry of Finance in Cryptocurrency Regulation

The Ministry of Finance is the primary authority responsible for crypto regulations in India. It decides how cryptocurrencies are classified and how they are taxed. Key responsibilities include:

- Defining crypto as a Virtual Digital Asset (VDA)

- Imposing 30% tax on crypto income

- Introducing 1% TDS on crypto transactions

- Drafting future crypto-related laws and policy frameworks

Whenever crypto tax rules are announced in the Union Budget, they come directly from the Ministry of Finance. This clearly indicates that crypto is recognized and regulated, not ignored or banned.

What Is RBI’s Role in Crypto Regulation in India?

The Reserve Bank of India (RBI) is responsible for maintaining India’s financial stability. RBI has consistently raised concerns about cryptocurrency due to:

- High price volatility

- Risks of money laundering

- Threats to monetary policy

- Lack of intrinsic value

While RBI does not directly regulate crypto trading, it strongly discourages its use as a currency. RBI also promotes the Digital Rupee (CBDC) as a safer alternative to private cryptocurrencies. In simple terms, RBI’s role is risk control, not taxation or trading regulation.

What Is SEBI’s Role in Crypto Regulation in India?

SEBI regulates traditional investment instruments such as stocks, mutual funds, and bonds. Currently, cryptocurrencies are not classified as securities, which is why SEBI does not directly regulate crypto markets. However, SEBI may play a future role if:

- Certain crypto assets are classified as investment products

- Exchanges are brought under a formal licensing system

- Investor protection rules are introduced

This is one reason crypto is treated differently from stocks in India.

Role of FIU-IND (Financial Intelligence Unit – India) in Cryptocurrency Regulation

FIU-IND plays a crucial role in crypto compliance. It monitors financial transactions to prevent: Money laundering, Terror financing and Illegal fund movement.

Crypto exchanges operating in India must: Register with FIU-IND, Follow strict KYC and AML rules and Report suspicious transactions.

This makes crypto transactions traceable and aligns India with global anti-money laundering standards.

Why Crypto Is Treated Differently from Stocks

Crypto is treated differently from stocks because:

- It is decentralized and not issued by any company or government

- Prices are highly volatile

- There is no central authority guaranteeing value

- Global transactions are harder to control

Stocks represent ownership in a registered company, while crypto is a digital asset with no physical backing. Due to these differences, India uses a separate regulatory and tax framework for crypto.

Crypto Tax Rules in India As of 2026

In India, cryptocurrency is taxed under a special category called Virtual Digital Assets (VDAs). The government has created separate tax rules for crypto, which are different from stocks, mutual funds, or other investments.

These tax rules apply even if crypto is not legal tender. If you make money from crypto, the government expects you to report and pay tax on it.

India imposes a flat 30% tax on income earned from cryptocurrency transactions. This tax rate applies to everyone, regardless of income slab.

What Crypto Transactions Are Taxed?

So now you might be wondering which crypto transactions are actually taxed. In simple terms, if you make money using crypto, the government considers it taxable. These crypto activities are taxable in India:

- Buying and selling cryptocurrency when you make a profit

- Converting one crypto into another, for example, Bitcoin to Ethereum

- Using crypto to pay for goods or services

- Receiving crypto as salary, payment, reward, or incentive

The rule is very simple if a crypto transaction results in profit, it is taxable, even if you don’t withdraw the money to your bank account.

No Loss Set-Off Rule

One of the strictest crypto tax rules in India is the no loss set-off rule. This means:

- Loss from crypto cannot be adjusted against profit from another crypto

- Crypto losses cannot be adjusted against income from stocks, salary, or business

- Crypto losses cannot be carried forward to future years

Only the purchase cost is allowed as a deduction. No other expenses are permitted.

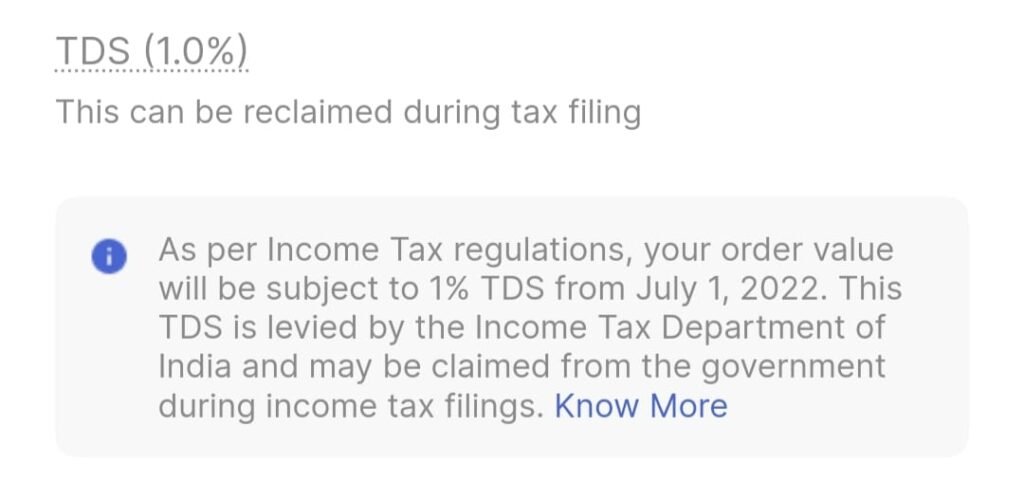

1% TDS on Crypto Transactions Explained

Apart from the 30% tax on crypto profits, India also applies a 1% TDS (Tax Deducted at Source) on certain crypto transactions. This rule often creates confusion, but in simple terms, it is mainly used by the government to track crypto activity, not to charge extra tax.

The 1% TDS is deducted at the time of selling crypto. This deduction happens regardless of whether you make a profit or a loss on the trade. In most cases, if you are using an Indian crypto exchange, the exchange automatically deducts the TDS on your behalf, so you do not need to do anything manually.

In peer-to-peer (P2P) transactions, the responsibility of deducting and depositing the 1% TDS falls on the buyer. If you trade through foreign crypto exchanges, the responsibility of complying with TDS rules may fall on the user, which makes proper record-keeping very important.

It is also important to understand that the 1% TDS is not an additional tax. According to platforms like CoinDCX, the TDS amount deducted can be claimed while filing your income tax return. It is adjusted against your total tax liability, similar to how TDS on salary works.

In short, 1% TDS reduces your available trading capital temporarily, but it can be recovered during income tax filing if you stay compliant.

How Crypto Salary from a Foreign Country Is Taxed in India (2026)

When you receive cryptocurrency as a salary in India, it is treated just like a normal salary income. The value of the crypto on the day you receive it is considered your income and is taxed according to your regular income tax slab.

The tax process begins at the time you receive the crypto itself. The fair market value (FMV) of the cryptocurrency on the date it is credited to you is considered your income. This amount is added to your total annual income and taxed under Income from Salary or Income from Other Sources, depending on the nature of the work.

Later, when you convert or sell that crypto into INR, a second tax event can happen. If the value of the crypto has increased during this period, the profit is taxed separately. In this case, a flat 30% tax applies only to the gain, not to the entire amount.

In simple terms, the calculation works like this: the selling price minus the value at the time of receipt gives you the profit or loss. If there is a profit, it is taxed at a flat 30% rate. If there is a loss, it cannot be adjusted or set off against any other income.

Let’s see this example : Value when received = ₹2,00,000

Sold later for = ₹2,50,000

Profit = ₹50,000

Tax = 30% of ₹50,000 = ₹15,000

Is Foreign Crypto Salary Legal in India?

Yes. Receiving salary in crypto from a foreign company is legal, but:

- It must be reported in your ITR

- You must pay applicable taxes

- Foreign income disclosure may be required

Not reporting it can lead to penalties and notices.

Risks of Ignoring Crypto Regulations in India

Ignoring crypto regulations in India can lead to serious financial and legal consequences. Many people assume crypto is anonymous or untraceable, but in reality, Indian authorities closely monitor crypto activities through exchanges, banks, and reporting systems. Non-compliance can cause long-term problems for example: heavy tax penalties, bank account freezing, Legal Notices from Authorities and Trading Restrictions.

If you want to better understand tokenized assets and real-world assets (RWA) and how they work in crypto, you can read our detailed guide here

Is crypto banned in India?

No, cryptocurrency is not banned in India. Indians are legally allowed to buy, sell, and hold crypto assets. However, crypto is regulated and heavily taxed, and it is not considered legal tender. This means crypto is allowed, but only under strict rules.

Can I hold crypto legally in India?

Yes, you can legally hold cryptocurrency in India. There is no law that prohibits owning or holding crypto. You are free to keep crypto in exchanges or private wallets, as long as you comply with tax and reporting requirements.

Is crypto income taxable even if I don’t withdraw it?

Yes. Crypto income is taxable even if you do not convert it to INR.

Is USDT legal in India?

Yes, USDT (Tether) is legal to hold and trade in India. However, like all cryptocurrencies, USDT is not legal tender and is subject to Indian crypto tax rules. Any profit made from trading USDT is taxable, and TDS rules may apply.

What happens if I don’t pay crypto tax?

If you do not pay crypto tax: You may receive notices from the Income Tax Department, Penalties and interest can be imposed, Bank accounts may be frozen for investigation, Exchanges may restrict or suspend your account and Ignoring crypto tax rules can create long-term financial and legal problems.

Nice article